Kenyan Courts and the Oversight of Transactions Involving Listed Companies

Updated guidance for boards, sponsors, and advisers on judicial restraint, minority shareholder risk, and defensible process in Kenyan capital markets transactions.

The judicial oversight of transactions involving publicly listed companies in Kenya is undergoing a quiet but significant shift. For much of Kenya’s corporate law history, courts adopted a posture of restraint intervening only where clear illegality, fraud, or contractual breach was demonstrated. Recent litigation signals a gradual recalibration: Kenyan courts are increasingly willing to scrutinise listed-company transactions where regulatory compliance, minority shareholder protection, and public interest are implicated.

Key point: Courts may avoid disrupting markets at the interim stage, but listed-company transactions are not immune from judicial scrutiny where credible regulatory or constitutional issues are raised.

Contents

- Context: the courts’ historical restraint

- The Diageo–EABL petition as a lens

- Interlocutory posture: restraint vs scrutiny

- What Kenyan courts are increasingly willing to scrutinise

- Minority shareholders and “quasi-public” listed companies

- Practical guidance for boards and deal teams

- Key references

- FAQ

1. Context: The Courts’ Historical Restraint in Commercial Matters

Kenyan jurisprudence has long recognised the need for judicial caution in commercial matters. Courts have consistently warned against undue interference with market activity particularly where such interference may disrupt commercial certainty or investor confidence. This principle remains intact.

The practical logic is straightforward: interim orders can effectively determine a transaction before parties are fully heard, and can create market instability especially where listed securities and dispersed investors are involved.

2. The Diageo–EABL Petition as a Lens on Capital Markets Oversight

The petition challenging Diageo Plc’s proposed disposal of its majority shareholding in East African Breweries Limited (EABL) provides a useful lens through which to examine the courts’ emerging role in capital markets oversight in Kenya.

The impugned transaction concerns the proposed disposal by Diageo Plc of its controlling interest in EABL — a company listed on the Nairobi Securities Exchange (NSE). A petition was lodged seeking, among other reliefs, orders restraining the transaction on grounds of alleged non-compliance with statutory and regulatory requirements governing changes in corporate control of listed companies.

3. Interlocutory Posture: Judicial Restraint Does Not Equal Abdication

At the interlocutory stage, the High Court declined to grant prohibitory relief and instead postponed the hearing for further directions. While no determination was made on the merits, the Court’s approach is instructive in understanding contemporary judicial attitudes toward complex commercial transactions involving listed entities.

By declining to issue immediate restraining orders, the Court reaffirmed the importance of preserving transactional stability pending a full hearing.

However, restraint does not equate to abdication. The Court’s willingness to entertain the petition and defer the matter for further consideration underscores a clear recognition: transactions involving listed companies are not immune from judicial scrutiny particularly where allegations of regulatory non-compliance or constitutional violations are raised.

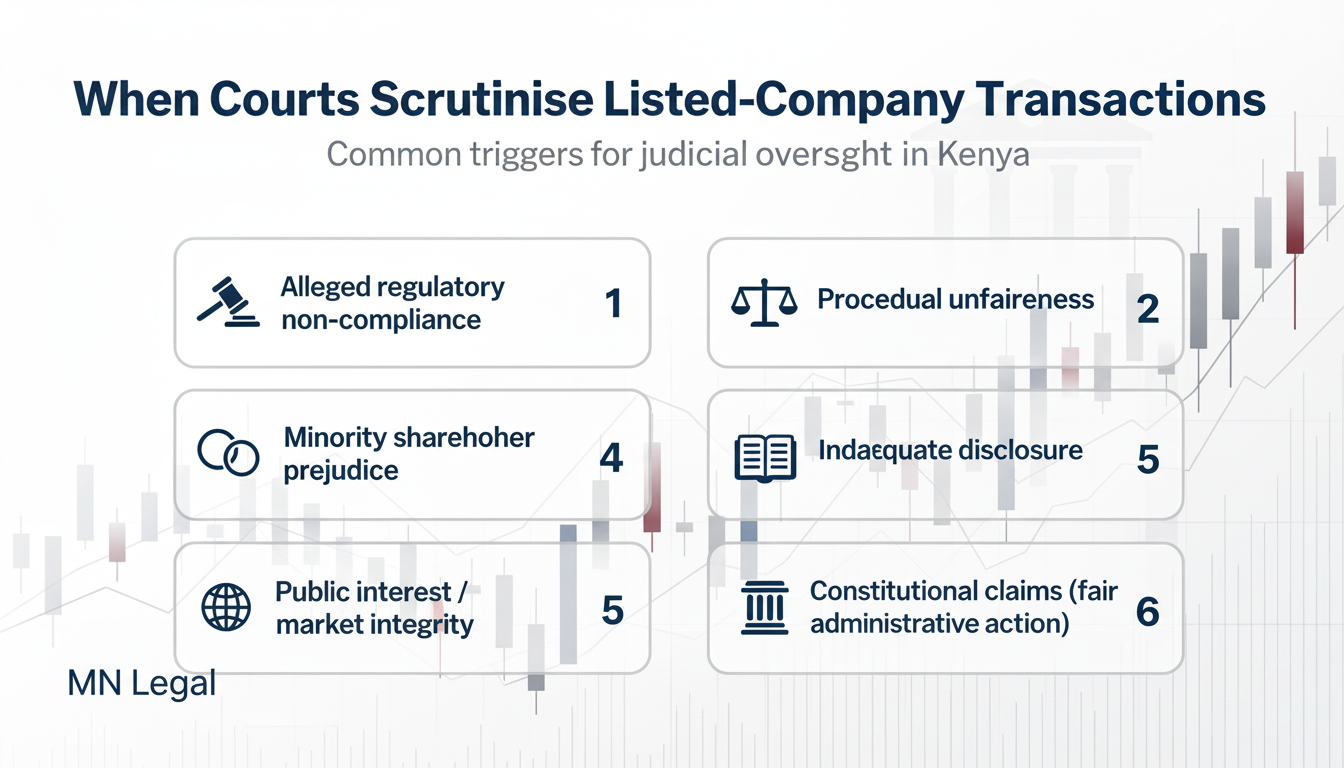

4. What Kenyan Courts Are Increasingly Willing to Scrutinise

A notable feature of recent litigation is the increasing justiciability of corporate transactions traditionally regarded as private commercial affairs. Kenyan courts have demonstrated readiness to interrogate:

- Compliance with capital markets and corporate governance regulations

- Procedural propriety in the obtaining of regulatory approvals

- Protection of minority shareholder interests

- Constitutional principles including transparency, accountability, and fair administrative action

5. Minority Shareholders and the Quasi-Public Nature of Listed Companies

The Court’s approach suggests that regulatory compliance is no longer viewed as an exclusively administrative concern it is one capable of judicial evaluation where public interest considerations arise.

The growing prominence of minority shareholders in litigation involving listed companies marks a significant development in Kenyan corporate law. Courts appear increasingly receptive to arguments that transactions affecting control of listed entities engage broader public and investor interests beyond the contracting parties.

This trend aligns with constitutional values and the evolving understanding of corporate governance in capital markets, where listed companies occupy a quasi-public position by virtue of their dispersed ownership and market participation.

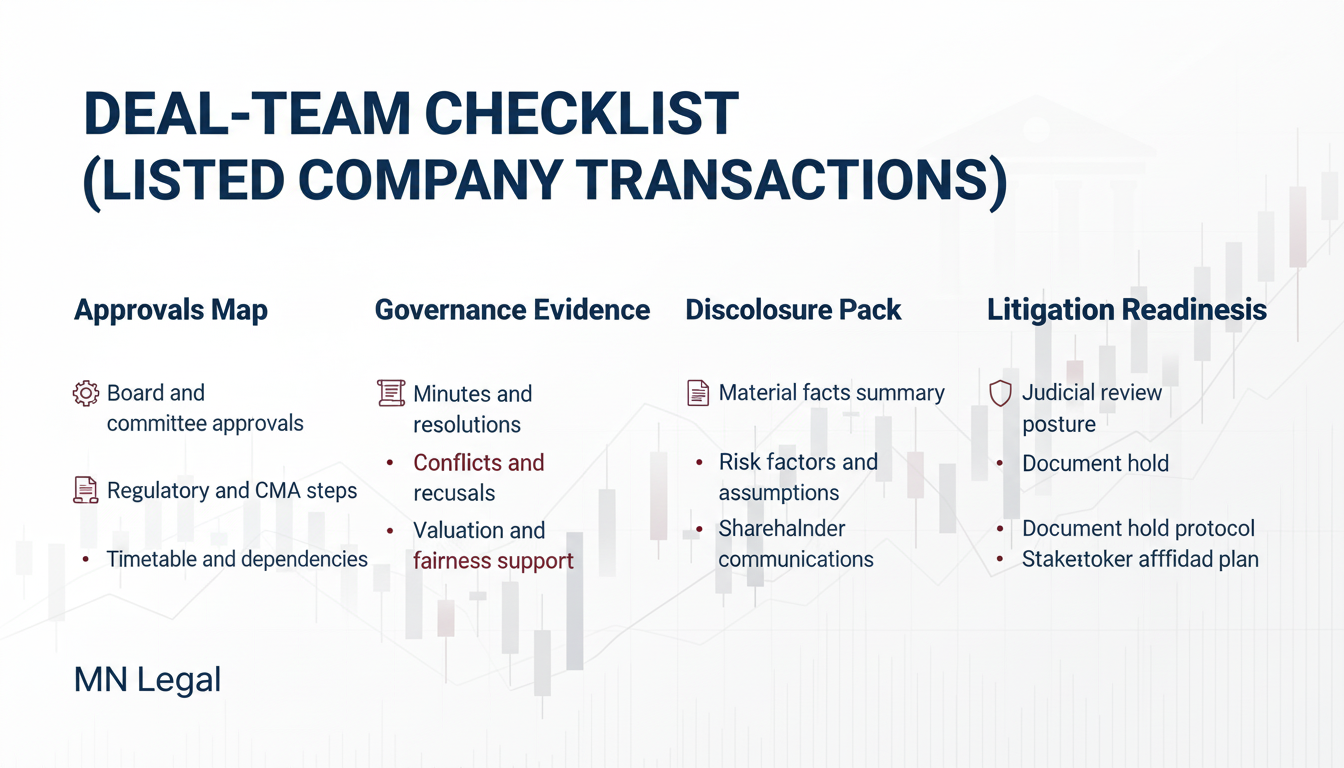

6. Practical Guidance for Boards and Deal Teams

The takeaway for deal teams is not that courts will routinely stop transactions. It is that deal documentation and process should be built to withstand scrutiny if challenged.

A) Build an Approvals Map Early

- Document the approvals pathway board, shareholder, and regulator steps where applicable.

- Maintain a clean record of submissions and key decision points.

- Align internal authorisations with transaction timelines and disclosure obligations.

B) Treat Governance Evidence as Deal-Critical

- Keep board papers and minutes that show rationale, risk consideration, and oversight.

- Document how conflicts are identified and managed.

- Maintain a single deal file with supporting evidence — not scattered email threads.

C) Plan for Minority Shareholder Scrutiny

- Stress-test fairness and disclosure arguments before announcements are made.

- Ensure communications are consistent across channels and documents.

- Anticipate interim applications and prepare a defensible narrative of compliance and process.

Need Deal Counsel on a Listed-Company Transaction in Kenya?

MN Legal advises on transaction structuring, approvals pathways, governance documentation, and litigation risk management for transactions involving regulated or listed entities in Kenya and across East Africa.

Make an enquiry | Explore Practice Areas

Key References

Related MN Legal pages: Practice Areas and Contact.

Frequently Asked Questions

Can Kenyan courts stop a transaction involving a listed company?

Yes, courts can grant interim or final relief in appropriate cases. They generally exercise caution to avoid destabilising markets, but may intervene where credible illegality, regulatory non-compliance, or procedural unfairness is alleged.

Does regulatory approval prevent court scrutiny of a listed-company transaction?

Regulatory approval is significant, but it does not automatically insulate a transaction from challenge — especially where constitutional principles or procedural fairness issues are raised.

Why are minority shareholders increasingly relevant in listed-company disputes in Kenya?

Listed companies have dispersed ownership and broad public participation. Kenyan courts may treat certain control-related transactions as implicating wider investor and market integrity concerns beyond the contracting parties.

What documentation reduces litigation risk in listed-company transactions?

A defensible approvals map, clear board papers and minutes, consistent disclosures, and a complete record of compliance steps and key decisions are often critical to withstanding challenge.

What is the biggest interim-stage risk for deal teams in Kenya?

Interim applications that delay closing or disrupt markets. Strong process evidence and consistency in disclosure reduce vulnerability to urgent injunctive relief at the interlocutory stage.

When should legal counsel be engaged on a listed-company transaction in Kenya?

Early during structuring and approvals planning. Early involvement improves process quality, reduces rework, and strengthens the defensibility of the transaction record.

Disclaimer: This case comment is provided for academic and professional discussion only and does not constitute legal advice.