The most commercially successful legal-tech products in capital markets are often the least dramatic: tools that help licensed

intermediaries keep clean records, onboard investors efficiently, deliver disclosures with audit trails, and demonstrate compliance

during due diligence.

Yet licensing questions arise precisely because these products sit close to the regulatory frontier. A platform may be built as

“workflow software” and still be treated as a regulated service if, in substance, it gives investment recommendations, arranges

transactions, holds client money, or functions as part of the public offering machinery.

Executive summary: Capital markets regulators tend to apply a functional approach. If your platform performs, controls,

or materially influences regulated activity, licensing or a licensed partner model may be required, regardless of how the product is marketed.

The licensing perimeter: the standard regulators apply

Across most capital markets regimes, licensing is not triggered by a company’s branding (“we are a technology company”) but by what

the company does. This is sometimes described as a substance-over-form or functional approach.

In practical terms, the perimeter tends to tighten around four activities:

(i) giving investment advice or making personalised recommendations,

(ii) arranging, placing, routing, or executing transactions,

(iii) handling client money, securities, or custody-like flows, and

(iv) facilitating public offering communications in a way that creates mis-selling or disclosure risk.

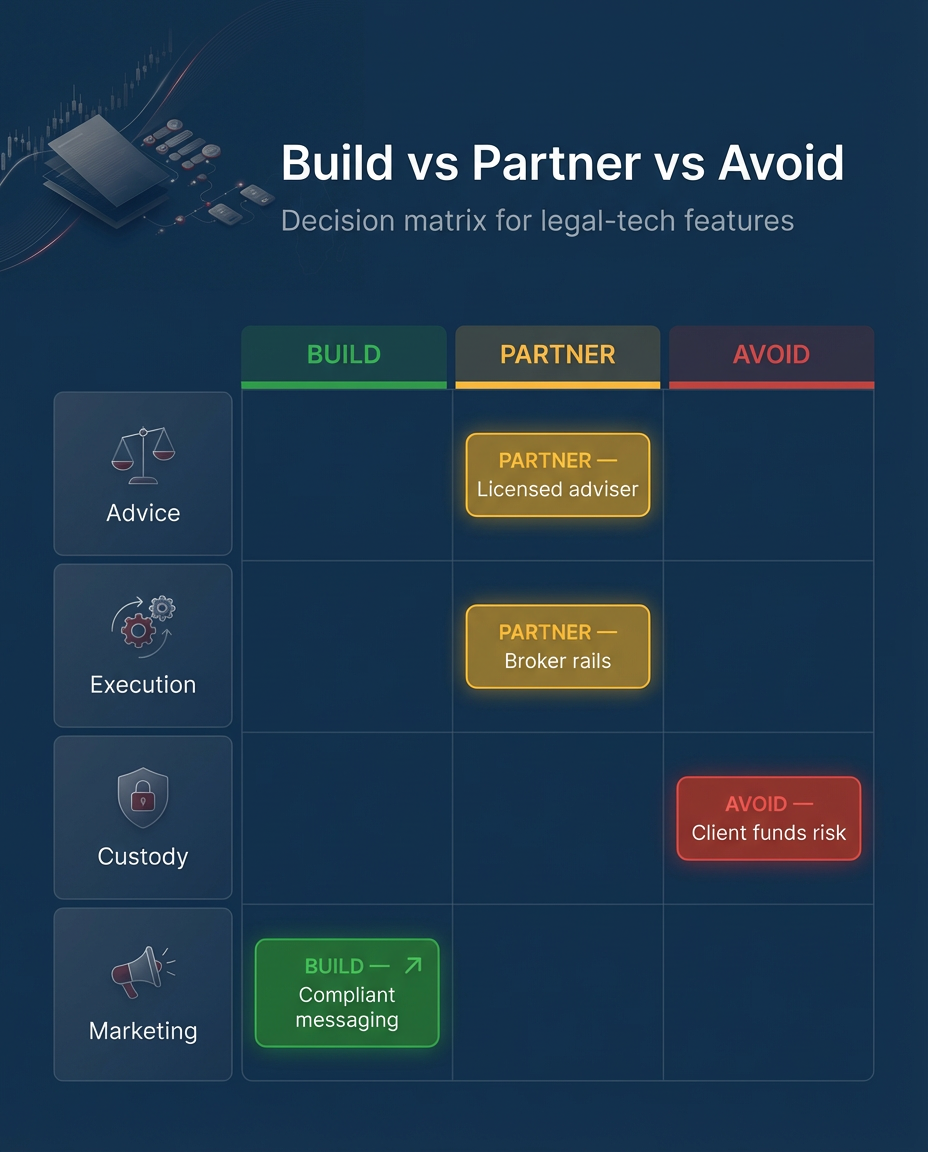

Legal-tech tools can sit safely outside the perimeter when they operate as internal compliance infrastructure for a licensed intermediary

and remain subject to clear boundaries: the tool supports, records, and evidences; the licensed entity decides, approves, and executes.

Where legal-tech products typically trigger perimeter concerns

Licensing risk most often appears not in a single feature, but in the way features combine into a workflow. Products designed for

investor onboarding, digital disclosures, and transactional workflow can become “front office” infrastructure very quickly.

Onboarding, disclosures, order flow, and custody-adjacent design are the most common perimeter pressure points.

Investor onboarding and eligibility

KYC and onboarding tooling is generally defensible when it remains a controlled workflow with clear oversight. Risk escalates when

the platform begins to make final determinations (who may invest, what products are suitable) without the licensed intermediary’s

meaningful review, or where the “profiling” output becomes a de facto recommendation.

Digital disclosures and investor communications

Digital disclosure tools are often low-risk, and highly valuable, when they solve the evidence problem: document versioning,

distribution logs, acknowledgements, and audit trails. Concerns arise where communications drift into promotion of an offer to the

public without adequate controls, or where disclosures are delivered without traceable evidence of what the investor received and when.

Order and transaction workflows

Interfaces that display information are one thing; workflows that route orders, “match” investors to opportunities, or control

execution logic may look like arranging or execution activity depending on the jurisdiction and the facts.

Custody, payments, and settlement-adjacent flows

Products that touch client funds directly or through accounts the platform controls require particular care. Even where a third-party

payment provider is involved, the question regulators ask is who controls the flow and who bears responsibility for safekeeping.

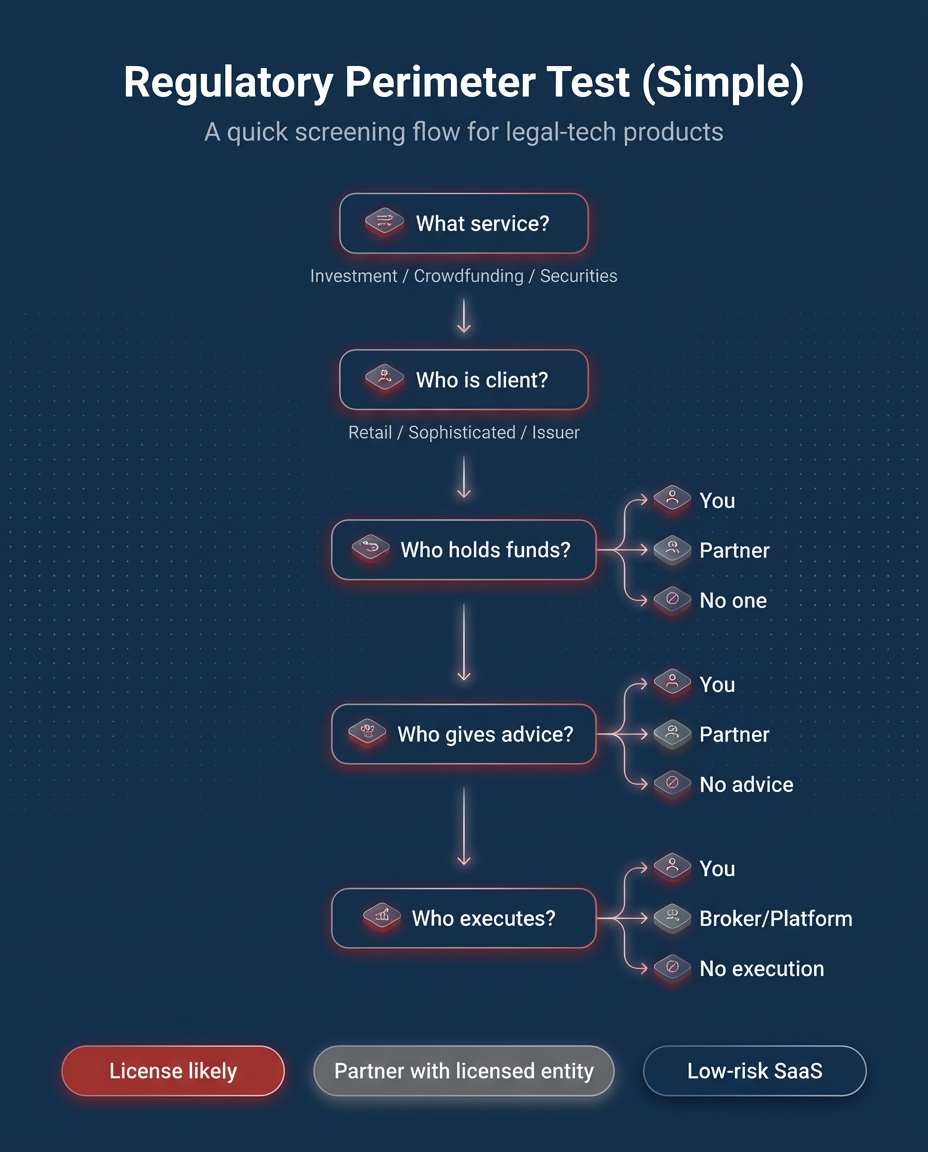

A practical perimeter test for founders and buyers

The most efficient way to avoid late-stage licensing surprises is to run an early perimeter test and write down the conclusion.

Think of it as a short internal legal memo that you can update at every major release.

The test is deliberately plain. It asks: what service is the product enabling; who is the client; who touches money; who influences

decisions; who executes; and who controls the communications. If the honest answers point toward advice, arranging/execution, custody-like

flows, or public offer facilitation, then the product should be structured around a licensed entity either by obtaining the relevant

permissions or by partnering with a licensed intermediary and allocating responsibilities clearly.

Designing for compliance: standards that travel across jurisdictions

Legal-tech teams operating internationally need principles that work across regimes even where definitions differ. The following

standards tend to be robust:

First, keep regulated functions with the licensed entity where required. Second, build systems that generate evidence: approvals,

versioning, acknowledgements, exception handling, and user action logs. Third, ensure that governance is not merely documented,

but operational meaning there are named owners, review points, and the ability to demonstrate what happened in a specific investor journey.

The strategic benefit is commercial as much as legal. Strong evidence and clearly bounded operating models reduce friction in procurement,

accelerate partner onboarding, and make regulatory discussions more orderly.

A realistic scenario: when “crowdfunding software” becomes a regulated service

Consider a platform built initially to support issuers with document workflows: issuer onboarding, disclosure templates, and investor

acknowledgements. The tool performs well and demand grows. Then the roadmap adds convenience features: investor “matching,” automated

eligibility approval, and in-platform collection of funds “to simplify settlement.”

Each feature looks incremental. Collectively, the platform may now resemble the machinery of a public offer and transaction facilitation.

At that point, the perimeter question becomes unavoidable: is the platform merely enabling a licensed intermediary, or is it effectively

arranging participation, influencing investment decisions, and controlling flows that look custody-adjacent?

The fix is usually not a full rebuild. It is a structural decision: allocate regulated steps to a licensed partner (or obtain the

necessary permissions), revise workflows to ensure meaningful oversight, and strengthen disclosures and records so the investor journey

is defensible.

Governance and documentation: what sophisticated partners will ask for

Intermediaries, institutional partners, and sophisticated clients increasingly require evidence of regulatory thinking. A premium posture

is to maintain a living file that includes: a perimeter memo, a feature risk register, an operating model diagram, vendor allocations,

and a compliance evidence map (what logs exist, who reviews them, and how exceptions are handled).

This is where legal-tech has an advantage. Unlike traditional paper processes, well-designed systems can produce reliable logs and

demonstrate accountability. The goal is not to generate paperwork; it is to make compliance auditable.

How MN Legal helps

Perimeter advice, partner models, and defensible product workflows

MN Legal advises legal-tech founders and capital markets intermediaries on regulatory perimeter mapping, licensing and partnering

structures, disclosure and onboarding workflow design, and the contractual allocation of responsibilities between platforms and

licensed entities. Where appropriate, we also support incident readiness and records strategy so your compliance posture is

evidenced not assumed.

External reference points that inform global standards include

IOSCO (securities regulation principles),

FATF (AML/KYC expectations),

and market regulators such as

ESMA and the

FCA.

FAQ

Does every investment or crowdfunding tool require licensing?

No. Many tools remain outside the perimeter when they are genuinely internal compliance or recordkeeping infrastructure for a licensed

intermediary. Risk depends on function and control particularly advice, arranging/execution, custody-like flows, and public communications.

What features most often create licensing pressure?

Personalised recommendations, investor matching/placement functions, order routing or execution logic, custody-adjacent payment flows,

and public offer communications without robust controls.

How should international legal-tech teams manage multi-jurisdiction uncertainty?

Start with consistent standards: a perimeter memo, a feature risk register, a partner model where regulated steps are performed by

licensed entities, and strong evidence (audit trails, disclosure versioning, acknowledgements, exception workflows).

Disclaimer: This article is general information and not legal advice. Licensing requirements vary by jurisdiction and facts. For advice on your specific model, contact MN Legal.